Beer on the Economy

September 2014

The UK recovery to date

The UK economic recovery is continuing, with GDP growing 0.8% in the first two quarters of this year. Recent PMI survey data also points to growth at a similar pace; although manufacturing expansion may have eased, the services and construction sectors continue to grow strongly.

That said, statistics at best give us a guide. It's not until many years have passed that we have an accurate idea of how the economy behaved. That point is being emphasised this month by large revisions to GDP data by the Office for National Statistics, partly due to changes in methodology. I highlighted the expected changes, and challenges for Labour,

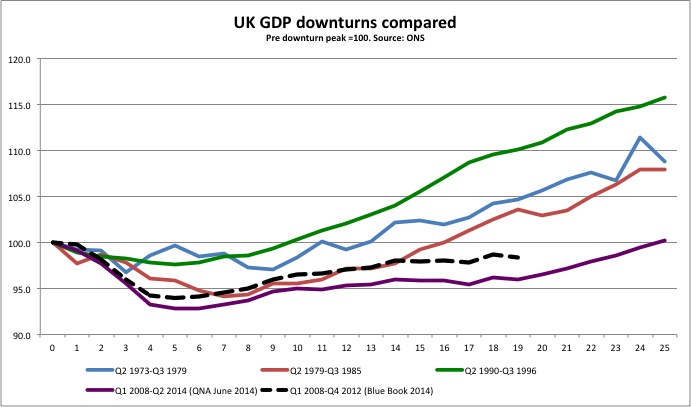

here. The latest revision (see chart) suggests the recession was shallower than previously thought.

The purple line shows the current recession and recovery. The dashed line shows the revised version of events. The UK economy is now thought to have contracted by 6% rather than by 7.2% as previously thought.

A casual glance at the chart also seems to indicate that from 2012 the economy has grown as a similar rate to previous recoveries - it's just that two years have been lost, from 2010 to 2012. Austerity policies, at home and in the Eurozone, must carry much of the blame. In 2010, economic policy went backwards. In the UK, that corresponded with the beginning of Conservative-LibDem government.

The most recent GDP data is also due for revision. The new figures are released on 30 September.

The ONS reports that GDP per person was revised up slightly but still remains 5.1% below the pre-recession peak, indicating that living standards have some way to recover. The average wage is hardly growing at present, and even though inflation is relatively low it remains higher than wage growth. The recession has had profound effects on people's lives, as highlighted in

a recent book I reviewed.

Productivity has been revised up a bit too, but the message is still the same. By the end of 2012, productivity was 12% below its pre-crisis trend (previously assumed to be 14% below).

More immediately, the approaching referendum in Scotland is likely to be having some impact on economic confidence, especially given recent opinion polls. Beyond the short term, the impact will depend on how the aftermath of the vote (whichever way it goes) is handled.

The battle for economic credibility

The next election will be in large part a battle of

economic credibility. The Conservatives and LibDems will struggle to explain why they have done so little to make sure more people benefit from recovery. Labour will need to show how it has rebuilt its economic credibility.

In this regard, I believe the

zero-based spending review to be one of the most important projects Labour is undertaking. It is vital we regain trust on spending, no matter what the arguments are about spending before the crisis. Our pledges on tax and spending

need to be consistent with our cost of living campaign. Some sort of

Effective Spending Guarantee should be considered. The basic theme should still be one of investment in our future, as outlined in

The Credibility Deficit.

Labour defence

Economies are subject to geopolitical risks, which are hard to predict. Certainly, the importance of getting it right on defence and national security has been clear over the past few weeks. In articles for Progress recently, I've outlined the need for

a deeper debate about defence in Labour, including how we can make spending more effective. There has been

an abdication of leadership in the Coalition so far. Labour needs to

build on its defence review and construct a distinctive defence policy, with more thought about the ethics of defence.

September 2014, 10/09/2014