Inflation and UK economic policy: some (obvious?) things to expect, and investment and ESG questions

Recent UK economic data mostly affirms the current grim outlook. Indeed, those feelings are evident in the latest GfK survey which shows consumer confidence at the most pessimistic since the survey began in 1974.

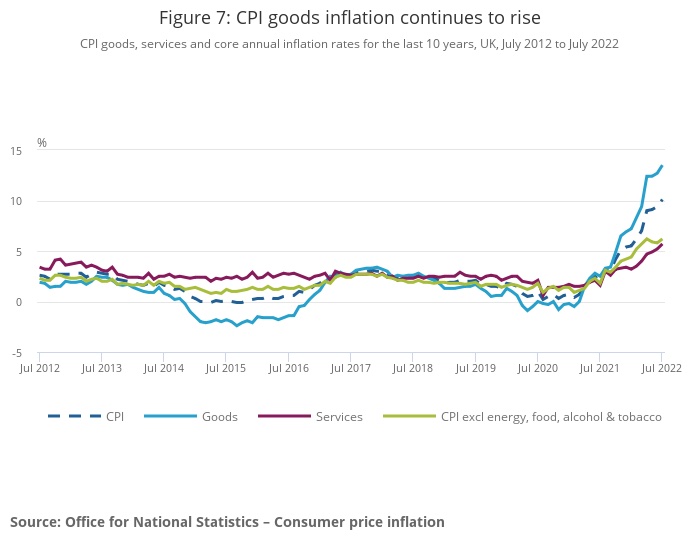

This is not surprising because the inflation rate continues to rise. Latest forecasts suggest it could approach 20% if the latest spike in gas prices prevails. CPI inflation is now running over 10%, with inflation rising across the different sectors in the economy. To a large extent this is driven by energy and food prices but, worryingly, when these are stripped out, core inflation is running at around 6% (see ONS chart below). No wonder the Bank of England is worried. The S&P Global/CIPS flash PMI survey has the UK economy just above contraction with manufacturing at a 27 month low, with companies expressing caution about the outlook (although reporting rate of input cost inflation lower eg as metals prices have fallen).

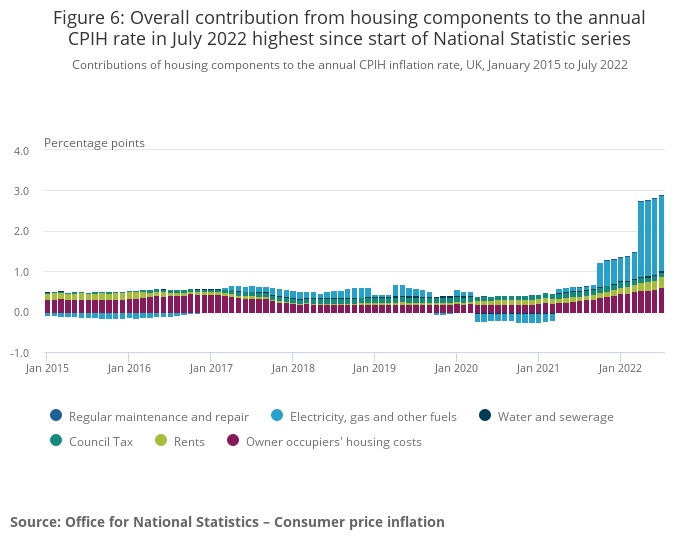

Rising prices in housing and household services are the main driver of inflation. That is mostly due to fuel price rises, as can be seen most clearly in the ONS chart breaking down the housing component of the CPIH index (actual housing cost elements are not included in CPI).

Looming on the horizon is an increase in the energy price cap for households and further rises in the Bank interest rate, perhaps by 0.5% in September given that consumer spending appears more robust than expected. Gilt yields have risen accordingly, with other markets also reflecting expectations of more hawkish central bank behaviour.

Here are some things we can expect:

-

The cost of living crisis is so bad, something will be done

Rising energy bills are hurting a large number of people particularly badly, with many already struggling to pay their bills. The expected new energy price cap, effective from October, will increase the harm. Income available for other things, such as clothing, holidays, etc will fall as heating homes eats household incomes.

Until the past few days, the assumption has been that events are outside anyone’s control. But politics always kicks in when things are really bad, overturning conventional wisdom. We saw this in the Global Financial Crisis and in the pandemic. Something will be done in this case too. The new Prime Minister will take action of some sort, whatever is being said today, to compensate people for higher bills, lower the cap (and compensate energy supply companies), or some combination. In ‘one’ sense, the outlook for consumers is therefore better than a week or so ago. And there will be pressure to do something for businesses, which are not protected by a price cap.

-

Fiscal action is possible but government spending, taxation, and borrowing will rise

The Institute for Fiscal Studies ran the numbers on the outlook for the public finances based on the Bank of England’s latest Monetary Policy Report, comparing it with the figures in the March Economic and Fiscal Outlook produced by the Office for Budget Responsibility (the fiscal watchdog). Factoring in new projections for inflation and growth leads to higher spending (eg on benefits) but over the next couple of years higher tax too (wages and prices rise and are taxed in nominal terms). The result is the fiscal headroom vs the government’s fiscal rules is pretty much unchanged (eg £30 billion approx before later support for energy bills).

The fiscal rule here (balancing the current budget) is a rolling target so in just over 6 months’ time the government will have another year to play with. In reality, the government will allow more borrowing short term to deal with the current crisis. It may even suspend fiscal rules given the extraordinary circumstances.

-

The Bank of England will take the opportunity to raise rates…

The Bank has been under a lot of fire recently. It certainly bears some of the responsibility for the current inflationary conditions (not the higher commodity prices, but the conditions which mean price rises are being passed on more easily), as I have highlighted previously. Now, while government works out what to do, but with fiscal action likely, the MPC is likely to take the view it should get on and raise rates further, so it has more scope to lower later. That approach may not be optimal, but it certainly may be politic.

-

…but rate rises now will have limited impact

Raising interest rates has some immediate effects. Depending on market expectations, it can move gilt yields across the curve (ie longer term interest rates). Variable mortgage rates change quickly. However, the Bank itself has acknowledged that changes in its Bank Rate take longer to affect the economy than used to be the case. This is largely because more people are on fixed term mortgage rates, so they don’t see an immediate change to their mortgage bills. This is not new news. Yet it does not seem to have given any urgency to the MPC’s rate decisions over the past 18-24 months. So the rate rise this month, to 1.75%, is some way behind the curve and more so than would have been the case before the financial crisis.

-

The inflation rate will fall back

Already some key commodity prices are well off their highs. Gas is the exception. We can probably expect higher prices across the board for some time (and prices are more volatile at higher inflation rates). But in a market economy, price acts as a signal. There will be supply responses. Some foods may take a couple of harvest cycles; China will overcome the latest Covid wave. Others will be much longer eg certain metals. In the middle is energy. Energy has many sources – high gas prices will drive substitution and over time this will lead to better energy efficiency (as in the 1970s) and a higher contribution from renewables with storage. The key challenge is getting through the next year or so, without the core inflation rate rising too far.

A more depressing driver of lower prices, and lower inflation, is a slowdown brought about by lower demand as energy bills dominate spending.

-

Active Quantitative Tightening may make things worse

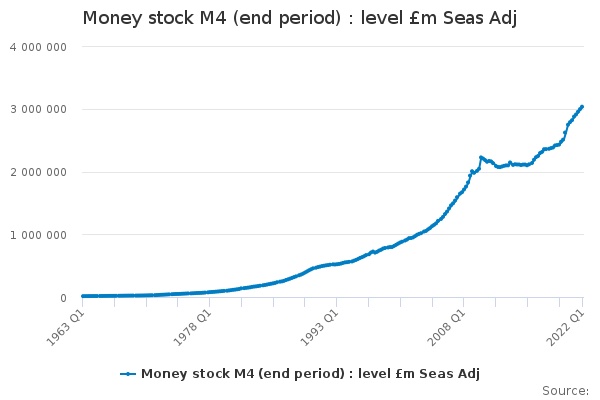

The Bank of England expanded its Quantitative Easing programme in the pandemic (pretty well matching the increase in government debt…). It continued to do so while the money supply expanded and even when it was clear the economy was recovering. Result? Probably higher inflation now than otherwise. Now, the Bank is starting to actively sell back the bonds it bought under QE. It will take measures to keep short term rates under control, but other things being equal the impact should lead to a fall in the money supply. Though the relationship is not direct in practice, this is likely to be disinflationary, at a time when the Bank is raising interest rates and when demand is being hit by rising energy prices (chart for illustration is from ONS).

QE after the financial crisis happened when banks were rebuilding their balance sheets, so the wider economy did not see a rise in money supply. Nor, as it happens, did it have inflationary conditions. Price shocks did push the inflation rate above 5% but wider inflation was limited.

What does the Bank expect to happen? It does not know. It does not consider the money supply when making monetary policy decisions. The view seems to be the link with inflation cannot in practice be predicted (the velocity of circulation of money is not stable), so there is little point. But arguably this view prevented the Bank coming to a wiser judgement a year or more ago.

-

Markets will…try to look ahead

While most people’s attention will be on the crisis here and now, markets will as always look ahead -discounting the bad news today. On an 18-24 month view the picture looks brighter (barring further geopolitical escalation) but as far as growth and productivity is concerned not that bright. Already we see attention drawn to expectations of recession. If QT does turn out to be disinflationary, asset markets themselves could be profoundly affected. Finding ways of sticking close to real economy exposure on reasonable valuations (not just based on past few years) amidst big sentiment swings will likely be a common pursuit (or a crowded trade?).

-

ESG implications not yet fully worked through

There has been much speculation about what this means for ESG investors but the debate still seems at an early stage. The most obvious impact will be on efforts to attain net zero. Greater use of more carbon intense fossil fuels appears likely to be the story for the next year or so. However, gas has now demonstrated it’s efficacy as a ‘transition’ fuel is limited if supply is not guaranteed (noting too of course the impact of methane leaks), so we should expect move to greater energy efficiency and substitution to other energy sources. A problem with renewables vs fossil fuels has been their lower return on investment and capacity to build out faster. Also, there are contradictory claims made about the ability to scale up battery storage for grids, including what if any technological developments and innovation are required. This is where we need higher quality information and some economics. There are considerable ESG implications for the extraction of transition metals and minerals, as I have written elsewhere. There are other ESG implications that shareholders should be clear about too, including on pay, employment, tax and global trade.

(updated 23/8/22)